How Much House Can I Afford With A $100,000 Salary Per Year?

To buy a house, you must follow the 28% rule and reduce your monthly expenses to save money and use it for a higher down payment.

Nov 10, 20231.2K Shares410.7K Views

Making $100,000 a year is a big step forward financially. If you're dreaming of owning a home, that income puts you in a good spot. But knowing exactly how much house you can comfortably buy takes more than just looking at your paycheck. Things like your debts, how much you've saved, your credit history, and the housing market where you want to live all play a big part.

Believe it or not, some studies show that even people earning over $100,000 are still living paycheck to paycheck. This just shows how things like higher prices for everyday goods and changing mortgage rates can make buying a house feel tough, even with a good income. To really figure out what you can afford, you need to look at the whole picture.

The 28/36 Rule Explained Simply

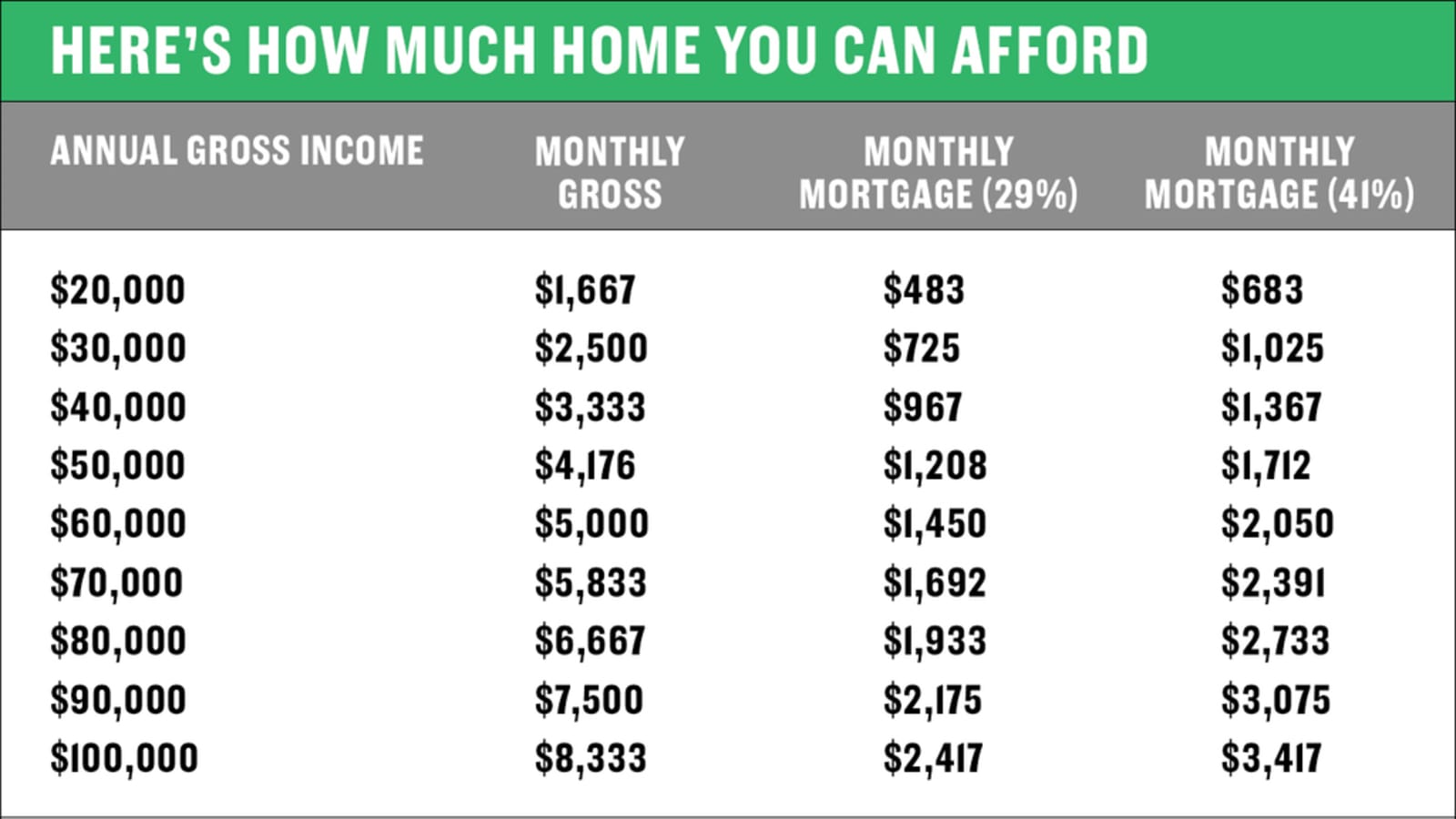

A common rule to help you budget for a home is called the 28/36 rule. Think of it this way: you shouldn't spend more than 28% of your total monthly income before taxes on all your housing costs. This includes your mortgage payment, property taxes, and homeowners insurance.

Also, all your monthly debt payments added together – that's your housing costs plus car loans, student loans, and credit card bills – shouldn't be more than 36% of your total monthly income before taxes.

So, if you make $100,000 a year, your monthly income before taxes is about $8,333. Following the 28% rule, your total housing costs should ideally be $2,333 or less each month. And according to the 36% rule, all your monthly debt payments together should be no more than $3,000. This rule is a good starting point, but everyone's situation is different, and the housing market can change, so it's not the only thing to consider.

Imagining The Possibilities - What Kind Of House Price Could Work?

Let's imagine you're looking at a $400,000 house and you've saved up a 20% down payment, which would be $80,000. If you got a 30-year mortgage with a 6.5% interest rate, your basic monthly payment for the loan itself would be around $2,022. This leaves you some room under that $2,333 guideline to cover property taxes, insurance, and maybe other fees. So, buying a $400,000 house might be possible with a $100,000 salary, depending on your other finances.

Now, what if you considered a $500,000 house? With the same down payment and interest rate, your basic monthly loan payment would jump to about $2,528. That's already more than the $2,333 guideline. This shows how even a slightly higher house price can make a big difference in your monthly costs and how much house you can comfortably afford.

How Can I Calculate How Much Home I Can Afford?

Estimating your affordable home price involves considering several key financial factors. Online tools like the Realtor.com home affordability calculatorcan provide a helpful starting point. To use such a calculator, you'll typically need to input the following information:

- Your Annual Income Before Taxes -This includes your base salary, wages, tips, and commissions, and can usually be found on your W-2 form. If multiple individuals in your household will contribute to the mortgage, their incomes should be combined.

- Your Total Monthly Debts -This includes all recurring monthly payments for loans (car, student, personal), minimum credit card payments, child support, and any other debts listed on your credit report. Importantly, this does notinclude living expenses like rent, groceries, or utilities.

- Your Available Funds -This is the total amount of money you have readily accessible for the down payment and closing costs. Examples include funds in bank accounts, personal loans, lines of credit, and investment accounts.

Once you enter this information into the Realtor.com affordability calculator and click "estimate home price range," it will provide an estimated home price range categorized as "affordable/fits your budget," "stretch/stretches your budget," and "difficult/over your budget."

Following this, you can utilize the Realtor.com free mortgage calculatorto estimate the monthly payments for a specific property you are considering. This tool allows you to input details like the home price, down payment amount, interest rate, and loan duration to determine the estimated monthly mortgage payment. A common guideline, as suggested by many financial experts, is to aim for a total monthly mortgage payment (including principal, interest, taxes, and insurance) that equates to 28% or less of your gross monthly income.

For a clearer example related to a $100,000 salary, assuming $62,500 saved for a down payment and closing costs and $650 in monthly debts, the Realtor.com calculator might estimate an affordable home price up to around $319,100. A home priced between $319,101 and $385,000 might be considered a stretch, while a home priced above $385,001 could be deemed over budget.

The $62,500 figure in this example is based on the typical upfront costs associated with a conventional $250,000 loan, including a 20% down payment ($50,000) to potentially avoid private mortgage insurance (PMI), and estimated closing costs (2% to 5% of the purchase price, or $5,000 to $12,500 on a $250,000 home) which cover fees like appraisal, title insurance, and lender fees.

Understanding your total monthly debts is crucial, as these obligations directly impact your ability to afford a mortgage payment. Your debt-to-income (DTI) ratio, calculated by dividing your total monthly debt payments by your gross monthly income, is a key metric lenders use to assess affordability.

A DTI of 36% or less is often considered affordable. For a $100,000 annual salary ($8,333 monthly gross income), this means aiming for total monthly debt payments (including the mortgage) of no more than $3,000, with housing-related expenses ideally below $2,333 (28% of gross monthly income).

How Much Is A Mortgage For $100,000?

The amount you'd pay each month for a $100,000 mortgage depends a lot on how long you take to pay it back (the loan term) and the interest rate you get. For example, if you have a 30-year loan with a 7% interest rate, your monthly payment for just the loan and the interest would be about $665.

If you chose to pay it off faster with a 15-year loan at the same 7% interest rate, your monthly payment would be higher, around $899, but you'd pay less interest in the long run and own your home sooner.

The interest rate you qualify for depends on things like the current state of the economy, decisions made by the central bank, and most importantly, your credit score. A better credit score usually means you'll get a lower interest rate, which will make your monthly payments lower and save you money on interest over the life of the loan.

Over the entire time you're paying off a $100,000 mortgage, the total interest you pay can end up being more than the original $100,000, especially with a longer loan. For instance, a 30-year, 7% mortgage could have you paying almost $140,000 in interest on top of the original loan, meaning you'd pay back nearly $240,000 in total.

On the other hand, a 15-year loan at the same rate would have much less total interest, around $62,000. So, when you're thinking about a $100,000 mortgage, it's really important to look at different loan lengths and interest rates to see what your monthly payments would be and how much the loan will cost you in total over time.

What Else Matters Besides Your Salary?

While your $100,000 income is a key factor, lenders will also look closely at other parts of your financial life to decide if they'll give you a mortgage and how much they'll let you borrow:

- Your Credit History and How Much Other Debt You Have -Your credit score is a big deal. A low score usually means higher interest rates on your mortgage, which makes your monthly payments higher and reduces how much house you can afford. Lenders also want to see how much other debt you have compared to your income. If you have a lot of car loans, student loans, and credit card debt, it might make them think you won't be able to handle a mortgage payment.

- How Much You've Saved for a Down Payment -The amount of money you can put down upfront is important. A bigger down payment means you need to borrow less money, which can lead to lower monthly payments and better loan terms. If your down payment is less than 20% of the house's price, you'll likely have to pay for private mortgage insurance (PMI), which is an extra monthly cost.

- Where You Want to Live and the Cost of Living There -The housing market is different in different places. The same $100,000 salary will buy you a lot more house in a less expensive area than in a big city where the cost of living is high.

- What You Really Need in a Home vs. What You Just Want -Think about what's essential in a house for you right now. If your main goal is just to stop renting and start building equity, a smaller, more affordable "starter home" might be a better option than trying to buy your dream home right away.

Navigating Financing Options

Prospective homebuyers should explore various mortgage financing options, including conventional loans, Federal Housing Administration (FHA) loans, Department of Veterans Affairs (VA) loans, and U.S. Department of Agriculture (USDA) 1 loans.

Obtaining mortgage pre-approval is a crucial step, providing a clear understanding of the loan amount a lender is willing to offer based on an individual's financial profile. Comparing offers from multiple lenders is advisable to secure the most favorable interest rates and fees. First-time homebuyer programs may also offer financial assistance with down payments or closing costs.

Strategic Considerations For Homeownership

If immediate homeownership appears financially challenging, focusing on strengthening savings and improving credit scores can enhance future affordability. Avoiding new debt and maintaining responsible credit behavior are essential during this preparation period. Consulting with a local real estate agent can provide valuable insights into the market and available properties within a realistic budget.

FAQs About Home Affordability

How Much Money Do I Need To Make To Buy A $500,000 House?

Let's break it down simply. If you put 20% down and get a typical 30-year loan, your basic payment could be around $2,500 a month. Once you add in things like taxes and insurance, that might go up to $3,000 a month, or $36,000 a year.

A common rule is to not spend more than about a third of your income on housing. So, to comfortably afford a $500,000 house, you'd probably need to earn at least $108,000 a year. Keep in mind, this is just a rough idea.

What Steps Can I Take To Potentially Afford A More Expensive Home In The Future?

Several strategies can help increase your home buying power. The most direct approach is to increase your income. However, improving your credit score can also significantly enhance affordability by enabling you to qualify for lower, more competitive interest rates on a mortgage.

Furthermore, actively working to reduce your existing debt can improve your debt-to-income ratio, which lenders view favorably and can increase the amount you are eligible to borrow.

What Is The Affordability Of A House In The US?

The middle price for a brand new single-family house across the whole United States is about $495,750. That means if you looked at all the new houses sold, half cost more than that, and half cost less.

Now, if you think about getting a mortgage with an interest rate of 6.5%, it turns out that about 77% of all families in the US (that's roughly 135 million families) can't actually afford a new house at that middle price.

What this really shows is that for a lot of people in America, buying a brand new house at the typical price is pretty difficult right now.

Final Words

Determining the affordable price range for a home with a $100,000 salary requires a holistic assessment of financial circumstances beyond just income. Factors such as creditworthiness, existing debt, savings, and the local housing market play integral roles.

Utilizing guidelines like the 28/36 rule and online affordability calculators provides a foundational framework, but a thorough evaluation of individual financial profiles and available financing options is essential for making informed home buying decisions.

Jump to

The 28/36 Rule Explained Simply

Imagining The Possibilities - What Kind Of House Price Could Work?

How Can I Calculate How Much Home I Can Afford?

How Much Is A Mortgage For $100,000?

What Else Matters Besides Your Salary?

Navigating Financing Options

Strategic Considerations For Homeownership

FAQs About Home Affordability

Final Words

Latest Articles

Popular Articles