How Much House Can I Afford With A $80,000 Salary Per Year?

The affordability of a home with an $80,000 annual salary requires careful financial planning and consideration of several factors.

Nov 09, 2023112.4K Shares1.7M Views

The desire to own a home, a place to build memories and establish roots, is a powerful one. If you're earning around $80,000 annually, you're in a strong position to pursue this dream. Navigating the path to homeownership requires more than just knowing your annual income.

It's about understanding the interplay of various financial factors, from your monthly budget to the intricacies of mortgage options, to ensure you find a home that fits comfortably within your financial means. Let's examine how to make that dream a reality with an $80,000 salary.

Understanding Your Financial Landscape

While an $80,000 annual income provides a solid foundation, the key to determining your true affordability lies in your net income, the amount you actually take home after taxes and other deductions.

For instance, with an $80,000 salary, your gross monthly income is approximately $6,666. However, after accounting for taxes, health insurance, and retirement contributions, your net monthly income might be closer to $5,000 or less. This net figure is crucial, as it represents the funds available for housing expenses and other financial obligations.

See Also: The Wealth Tax Imperative

The 28/36 Rule - A Compass For Affordability

A widely used guideline for assessing home affordability is the 28/36 rule. This rule suggests that your core housing expenses (principal, interest, property taxes, and homeowner's insurance) should ideally not exceed 28% of your grossmonthly income.

Furthermore, your total monthly debt, including housing costs, car loans, credit card payments, and other obligations, should remain below 36% of your gross monthly income. Applying this rule to an $80,000 annual salary (approximately $6,666 gross monthly income), your target housing expenses would be around $1,866 per month, and your total monthly debt should ideally be no more than $2,400.

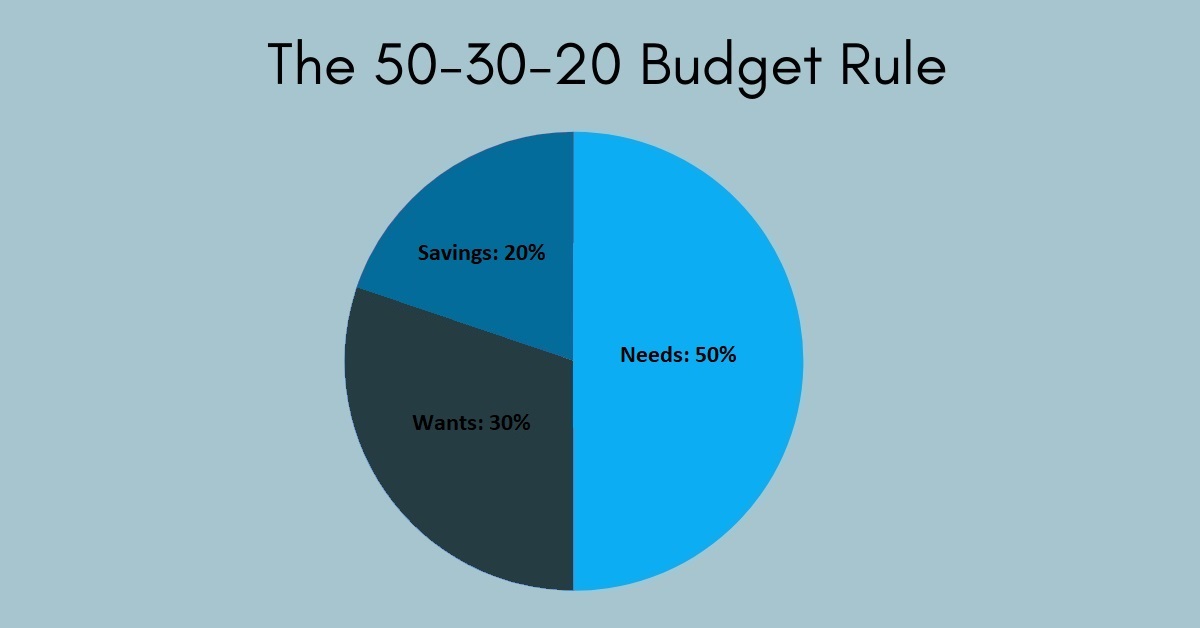

Budgeting Basics - The 50/30/20 Approach

Creating a solid budget is essential for prospective homeowners. The 50/30/20 rule offers a helpful framework: allocate 50% of your net income to needs (housing, transportation, food), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment.

While this is a general guideline, you can adjust the percentages based on your individual circumstances and financial priorities. For example, you might choose to allocate a slightly larger portion to savings if you're aiming for a larger down payment.

Preparing For A Mortgage - Credit Score And DTI

Two key factors that lenders consider when evaluating your mortgage application are your credit score and your debt-to-income ratio (DTI).A higher credit score demonstrates responsible borrowing behavior and typically qualifies you for lower interest rates. Aim for a credit score of 700 or higher to secure the most favorable terms. Your DTI, as mentioned earlier, is a measure of your monthly debt obligations compared to your gross monthly income. Lenders generally prefer a DTI below 43%, and ideally even lower, to ensure you can comfortably manage your mortgage payments.

Exploring Mortgage Options On $80,000 A Year

There are only two options for that person who earns $80,000 per year, and these are fixed and adjustable mortgages. Unfortunately, those mortgage plans will remain the same for people earning more or less than $80,000 annually.

Fixed Mortgage

The fixed mortgage is where you will have to pay the same interest rate every month because, according to this rule, you need to pay a high amount before purchasing any home, then the interest rate will remain the same for a lifetime or 30 years.

Adjustable Mortgage

If your monthly income is low according to your monthly budget, then I recommend you not go with this option. However, according to an adjustable mortgage, your interest will change after six months, but you have to pay a low amount before buying a home.

The Impact Of Interest Rates On Your Purchase Power

The interest rates significantly impact your purchasing power because if you pay higher interest rates for loans, mortgages and credit cards, you end up with your monthly income before a month.

It will significantly impact your purchasing power because you have to pay more money on interest rates, and it will also affect your credit scores. Buying a home is the dream of every person, and everyone wants a home in a good location; those people also try to buy a home in a good location with low-interest rates that will help them save some money on their monthly income.

Paying a high-interest rate will impact your buying power, and you will also have to face financial issues while having a $80,000 monthly payment.

Understanding Your Down Payment

The down payment is the critical step in buying a house, which is always around 20% of the home price. If someone earns $80,000 per year, that person can afford a home of approximately $310,000, and the down payment amount is around $6,2000. There are two types of down payment: if you pay a high amount for a down payment, you have to pay a low interest rate, and if you pay a low down payment, you have to pay a high interest rate.

Key Points To Note

- Larger down payment = smaller loan & lower monthly payments.

- Better interest rates are often offered with larger down payments.

- Less than 20% often requires Private Mortgage Insurance (PMI), an extra monthly cost.

- A larger down payment builds more immediate equity.

Strategically saving through budgeting, automation, and exploring assistance programs can help you achieve a comfortable down payment. Understanding these options is key to affordable homeownership.

The Real Cost Of Being A Homeowner

Owning a home goes far beyond just paying your monthly mortgage. While principal and interest payments are significant, they’re just one part of the bigger picture. To truly understand the financial commitment of homeownership, you need to account for property taxes, homeowners insurance, and most importantly ongoing maintenance.

Maintenance is where many new homeowners get caught off guard. A beautiful or even modestly-priced home will only stay that way with regular upkeep. Over time, every home needs repairs, it’s a leaking roof during the rainy season, peeling paint, worn-out appliances, plumbing issues, or exterior damage.

Even if you’ve bought in a great neighborhood or chosen a home that fits your lifestyle, neglecting maintenance can significantly hurt your property’s resale value. That’s why it’s smart to set aside a portion of your monthly budget, ideally 1% to 3% of your home’s value for routine maintenance and emergency repairs.

Read Also: Understanding Tax Reporting

Navigating First-Time Homebuyer Programs

There are programs like FHA loans, Conventional mortgages, VA loans, etc., but the FHA loan program is best for you if your annual income is not much higher or you have low credit scores.

It would be best to have high credit scores and low monthly expenses to avail of any program. Then, the FHA program is the best option. If you have a 580 credit score, you are eligible for an FHA loan, and if you have a higher credit score, you can go with multiple choices.

The Importance Of A Real Estate Agent

A skilled real estate agent can be invaluable in your home-buying journey. They have expertise in the local market, can help you find suitable properties, negotiate offers, and navigate the complex paperwork involved in a real estate transaction.

Reasons To Hire A Real Estate Agent

- They have a great experience of buying and selling home

- They offer several kinds of profitable offers

- Natural agents can get you home on MLS

- Real estate agents recommend a faster way to buy and sell your home

- They handle all the procedure

- They also offer you objective support

Long-Term Planning - House As An Investment

Beyond immediate comfort, homeownership is a significant long-term investment, building equity and potentially appreciating in value. Consider these factors:

Location: Desirable areas with good schools, safety, and amenities tend to see stronger, more consistent property value increases.

Market Trends: Staying informed about local and national housing supply, demand, and interest rate shifts helps you make strategic buying decisions for long-term gain.

Property Condition & Maintenance: Regular upkeep and timely repairs protect and can even enhance your home's value over time, impacting its investment potential.

Economic Factors: Local and national job growth and interest rate levels significantly influence housing demand and property prices.

Infrastructure & Development: New roads, schools, and commercial projects can make a location more desirable and boost nearby property values.

Your Financial Goals: Ensure your homeownership plans align with your broader investment strategy and long-term financial security.

FAQs About House Ownership

Will My Monthly Debts Affect How Much House I Can Afford?

Yes, lenders consider your debt-to-income (DTI) ratio. If you have student loans, car payments, or credit card debt, it will reduce the amount of home you can afford. A lower DTI ratio increases your chances of qualifying for a better loan and a higher home price.

What Kind Of Mortgage Should I Consider With An $80,000 Salary?

A fixed-rate mortgage is often best for stability, especially if you plan to stay in the home long term. However, if you expect your income to increase or plan to move within a few years, an adjustable-rate mortgage (ARM) might offer lower initial payments. Always compare options based on your financial goals.

How Much Should I Save For A Down Payment On A House With This Salary?

A typical down payment is 20% of the home's price, but many first-time buyers qualify for lower down payments (as low as 3% to 5%). On an $80K salary, aim to save at least $12,000 to $40,000, depending on the house price and loan type.

Why Are Property Taxes And Insurance Important To Consider?

These are recurring costs of homeownership in addition to your mortgage payment. Failing to budget for them can lead to financial strain and make it difficult to adhere to affordability guidelines like the 28% rule.

Final Words

The affordability of a home with an $80,000 annual salary requires careful financial planning and consideration of several factors. Income is necessary; other factors such as debt, credit score, and personal financial goals also play significant roles. Finding a balance between homeownership desires and maintaining a manageable debt-to-income ratio is crucial.

Ultimately, responsible budgeting and well-informed decision-making will ensure that purchasing a home remains a financially sustainable and fulfilling investment for those earning $80,000 annually. It depends on your lifestyle and what kind of house you want to buy, but always remember or calculate all the expenses before buying a home.

Jump to

Understanding Your Financial Landscape

The 28/36 Rule - A Compass For Affordability

Budgeting Basics - The 50/30/20 Approach

Preparing For A Mortgage - Credit Score And DTI

Exploring Mortgage Options On $80,000 A Year

The Impact Of Interest Rates On Your Purchase Power

Understanding Your Down Payment

The Real Cost Of Being A Homeowner

Navigating First-Time Homebuyer Programs

The Importance Of A Real Estate Agent

Long-Term Planning - House As An Investment

FAQs About House Ownership

Final Words

Latest Articles

Popular Articles